The United Arab Emirates is making a decisive leap toward digital governance and tax compliance with the introduction of a mandatory Electronic Invoicing System (EIS). This fundamental shift replaces traditional paper and simple PDF invoices with structured, machine-readable data, ushering in a new era of transparency and efficiency for every VAT-registered business.

This article provides a detailed breakdown of the UAE’s e-invoicing mandate, its technical requirements, the phased timeline, and how firms like Finexus are critical in ensuring a smooth transition to full compliance.

1. Defining True E-Invoicing: Beyond the PDF

Many businesses currently send invoices electronically via email as PDFs. However, the UAE’s new mandate defines an e-invoice far more stringently.

An E-Invoice in the UAE context is:

- Structured Data: The invoice is issued, transmitted, and received in a digital format (specifically XML or JSON) that is machine-readable and allows for automated processing.

- Mandatory Format: It must adhere to approved international standards adapted for the UAE, primarily PINT-AE (Peppol International for UAE).

- Secure Exchange: It must be transmitted securely through an Accredited Service Provider (ASP) connected to the specified network (based on the Peppol 5-Corner model).

- Real-Time Reporting: The invoice data is sent to the Federal Tax Authority (FTA) in near real-time, facilitating continuous transaction control.

Crucially, unstructured formats such as emailed PDFs, scanned images, or Word documents will no longer be considered valid tax invoices for in-scope transactions once the mandate takes effect.

2. Scope and Mandatory Implementation Timeline

The UAE’s Electronic Invoicing System is being rolled out in a phased approach, providing businesses with a clear schedule for preparation based on their size.

Transactions In-Scope:

The mandate primarily covers transactions between businesses and the government:

- Business-to-Business (B2B): All transactions between VAT-registered entities.

- Business-to-Government (B2G): All supplies made to government entities.

- B2C (Business-to-Consumer): These transactions are currently excluded but may be brought into the scope in future phases.

Phased Compliance Timeline:

| Business Category | Revenue Threshold | Deadline to Appoint ASP | Mandatory Go-Live Date |

| Pilot Program (Voluntary) | Selected taxpayers | N/A | July 1, 2026 |

| Large Businesses | AED 50 Million or more | July 31, 2026 | January 1, 2027 |

| Other Businesses (SMEs) | Less than AED 50 Million | March 31, 2027 | July 1, 2027 |

| In-Scope Government Entities | N/A | March 31, 2027 | October 1, 2027 |

Note: The deadline to appoint an Accredited Service Provider (ASP) precedes the mandatory implementation date, emphasizing the necessity of early technical preparation.

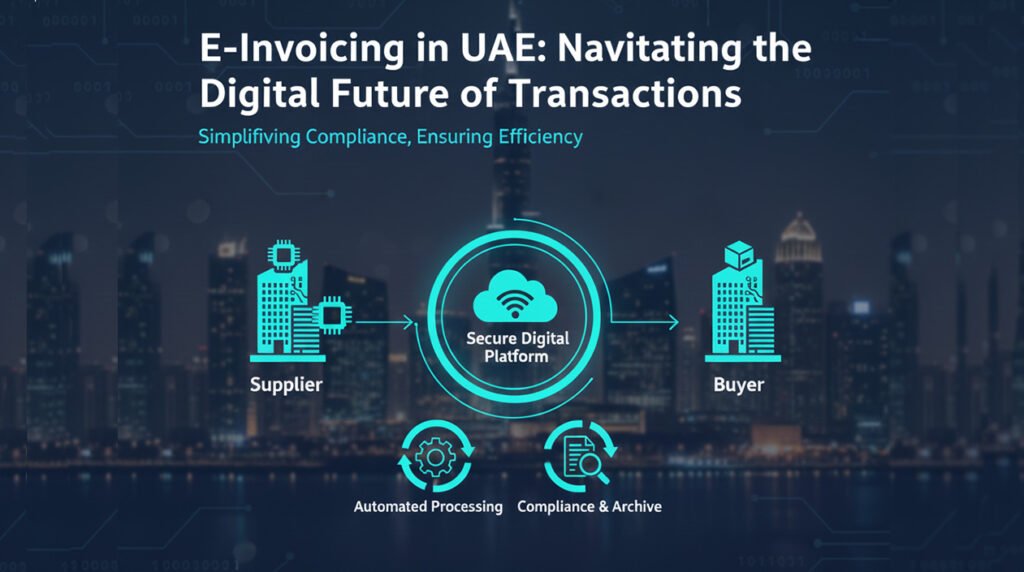

3. The Technical Architecture: Decentralized Peppol Model

The UAE has chosen a Decentralized Continuous Transaction Control and Exchange (DCTCE) Model, largely based on the global Peppol framework, often described as a “5-Corner Model.”

How the E-Invoicing Process Works:

- Supplier System (Corner 1): The supplier generates the invoice data in their ERP or accounting system, ensuring all required fields map to the FTA’s data dictionary.

- Sending ASP (Corner 2): The supplier’s system transmits the data to their Accredited Service Provider (ASP). The ASP validates the invoice data against all MoF/FTA rules, converts it to the mandatory XML/JSON PINT-AE format, applies a digital signature (to ensure integrity), and transmits it.

- Receiving ASP (Corner 3): The ASP uses the Peppol network to securely transmit the validated invoice to the buyer’s designated ASP.

- Buyer System (Corner 4): The buyer’s ASP receives the compliant e-invoice and delivers it directly to the buyer’s internal accounting system for automated processing.

- FTA (Corner 5): In parallel with the exchange between the supplier and buyer, the ASP sends a structured extract of the invoice data to the FTA’s central platform (Corner 5), providing near real-time visibility for tax monitoring.

This model delegates the heavy lifting of validation and exchange to the certified ASPs, ensuring high security (via encryption and digital signatures) and standardizing the data exchange across all businesses.

4. Critical Compliance Obligations

The mandate introduces several new non-negotiable obligations for VAT-registered businesses:

- Mandatory ASP Engagement: Both the invoice issuer and the recipient must appoint an MoF-accredited ASP to handle the transmission and reception of e-invoices.

- ERP/System Alignment: Internal accounting and ERP systems must be upgraded to generate invoices in the prescribed structured format (XML/JSON) and map all data fields accurately.

- Real-Time Reporting: Invoices and credit notes must be issued and reported through the system within the mandated timeframes (generally considered near real-time or within 14 days of the supply).

- Data Storage: E-invoices must be stored electronically within the UAE for the required statutory period (currently 5 years for most transactions).

- Error Reporting: Any technical failure preventing the issuance or receipt of e-invoices must be reported to the FTA within two business days.

By partnering with Finexus, you convert the regulatory burden of e-invoicing into a strategic advantage, guaranteeing compliance and unlocking the benefits of automated, error-free financial processing.